Corporate Sustainability Reporting: Why Transparency Matters

In today's interconnected world, sustainability isn't just a buzzword; it's a critical imperative. Consumers are demanding ethically sourced products, investors are prioritizing ESG (Environmental, Social, and Governance) factors, and employees want to work for companies that align with their values. Yet, amidst this growing awareness, a shadow of skepticism lingers. "Greenwashing," the practice of misleading consumers about a company's environmental practices, has become alarmingly common. This mistrust underscores the paramount importance of transparency in corporate sustainability reporting. But what exactly is it, and why does it matter? Corporate sustainability reporting is the process by which companies disclose their impacts and performance related to environmental, social, and governance issues. Transparency, in this context, is the act of providing clear, honest, and accessible information about these impacts. This blog post will delve into why transparency is the cornerstone of credible sustainability reporting and how companies can achieve it.

Defining Transparency in the Context of Corporate

Sustainability Reporting

Transparency, in its broadest sense, refers to the degree to

which information is accessible, understandable, and verifiable. In the context

of corporate sustainability reporting, it extends beyond mere disclosure to

encompass the quality and nature of that disclosure. While there is no

single definition of the term, the sustainability standards body, Global Reporting Initative (GRI) emphasizes transparency as the need for

organizations to disclose clear, accurate, and comparable sustainability

information.

Drawing from organizational theory and information

economics, transparency can be understood as:

§ "The

process of making organizational decisions, actions, and impacts known to

external stakeholders in a clear, open, and verifiable manner." (Adapted

from Hood, 2010, on governmental transparency, applied to corporate context).

§ It

involves reducing information asymmetry between the reporting organization and

its stakeholders, allowing for informed evaluation and accountability.

§ It

is not simply about releasing data, but about providing context, methodology,

and limitations, enabling stakeholders to understand the information's

significance.

Transparency is multidimensional, involving

- Disclosure: The act of making information available.

- Clarity: The ease with which information can be understood.

- Accuracy: The factual correctness of the information.

- Completeness: The comprehensiveness of the information provided.

- Verifiability: The ability of stakeholders to independently confirm the information.

In practical terms,

transparency in sustainability reporting means:

- Clearly

outlining the methodologies used for data collection and analysis.

- Disclosing

both positive and negative impacts, avoiding selective reporting.

- Providing

context for data, explaining trends and deviations.

- Making

reports easily accessible and understandable to diverse stakeholders.

- Subjecting

reports to independent assurance to enhance credibility.

- Being

open to stakeholder feedback and questions.

Why Transparency Matters in Sustainability Reporting

Transparency is fundamental to sustainability reporting as

it fosters trust and credibility. By openly sharing their ESG efforts and

outcomes, companies can build stronger relationships with investors, customers,

employees, and the wider community.

A. Building Trust with Stakeholders

- Trust is the bedrock of any successful relationship, and corporate sustainability is no exception. Transparent reporting builds trust with investors, who need reliable data to assess long-term risks and opportunities. Customers, increasingly conscious of their environmental footprint, want to support brands that are genuinely committed to sustainability. Employees, especially younger generations, seek employers whose values resonate with their own. By providing clear and verifiable information, companies demonstrate their commitment to accountability, fostering trust and loyalty. Conversely, a lack of transparency breeds suspicion. When companies obfuscate data or make vague claims, they risk being labeled as greenwashers, damaging their reputation and eroding stakeholder trust.

:max_bytes(150000):strip_icc()/https-www.investopedia.com-terms-a-accountability-primary-FINAL-2be10e089f5d42629803cea7885a023d.png)

- Transparency holds companies accountable for their sustainability commitments. When organizations disclose their performance metrics, they create a benchmark against which their progress can be measured. This allows stakeholders to assess whether a company is meeting its stated goals and fulfilling its promises. Meaningful comparisons and benchmarking become possible, enabling investors and consumers to differentiate between genuine sustainability leaders and those merely paying lip service.

- Transparency ensures companies provide accurate, verifiable, and balanced sustainability reports—reducing the risk of greenwashing (misleading sustainability claims).

C. Ensure Compliance with Regulations and Standards

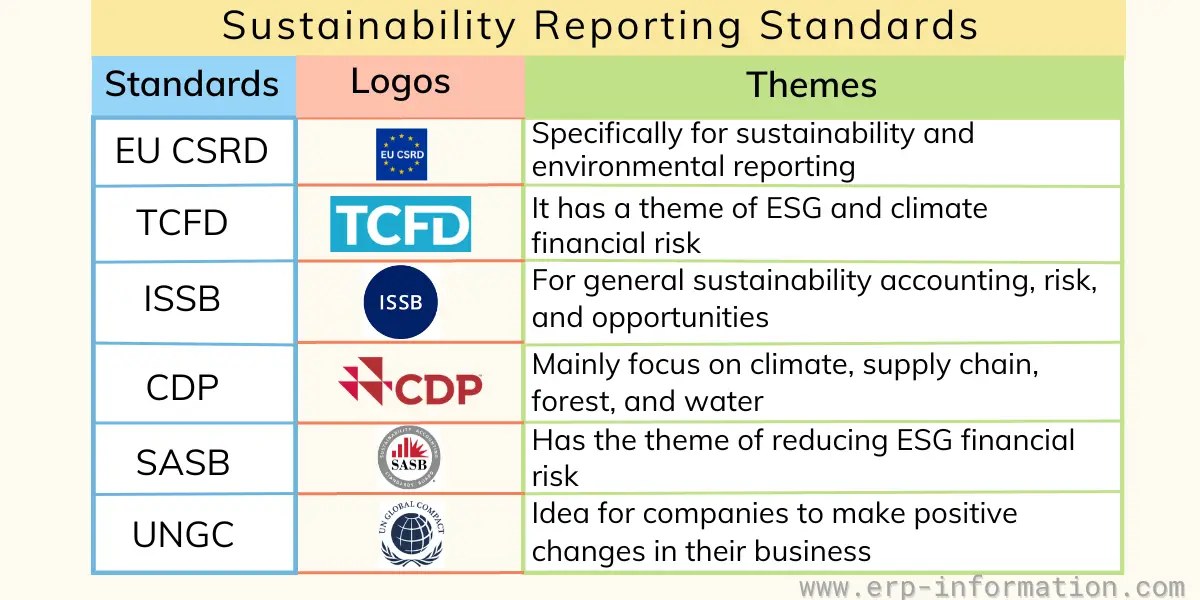

Transparency in sustainability reporting helps companies adhere to legal requirements and industry standards, reducing regulatory risks and strengthening corporate governance. Governments and regulatory bodies worldwide are increasingly mandating sustainability disclosures to ensure companies report their environmental and social impacts transparently. Some key regulations and standards include:

- Corporate Sustainability Reporting Directive (CSRD) – Requires large and listed EU companies to report detailed ESG disclosures using European Sustainability Reporting Standards (ESRS).

- U.S. SEC Climate Disclosure Rule (Proposed) – Would require publicly traded companies to disclose climate-related risks and greenhouse gas (GHG) emissions in their financial reports.

- UK’s Streamlined Energy and Carbon Reporting (SECR) – Mandates carbon and energy usage disclosures for large companies.

- Global Reporting Initiative (GRI) – Encourages companies to report sustainability impacts in a standardized and comparable manner.

- Sustainability Accounting Standards Board (SASB) – Provides industry-specific ESG disclosure guidelines for financial materiality.

- Task Force on Climate-related Financial Disclosures (TCFD) – Focuses on transparent climate risk reporting to guide investors and policymakers.

- International Sustainability Standards Board (ISSB) IFRS S1 & S2 – A global standard integrating financial and sustainability disclosures.

- Investors rely on accurate and comprehensive sustainability data to make informed investment decisions. Transparent reporting provides the necessary information to assess a company's environmental and social risks, as well as its potential for long-term value creation. Similarly, consumers need transparent information to make responsible purchasing decisions. Transparent reporting empowers stakeholders to make choices that align with their values and contribute to a more sustainable future.

E. Promoting Continuous Improvement:

- Transparency fosters a culture of continuous improvement. When companies publicly disclose their sustainability performance, they are incentivized to identify areas for improvement and implement corrective actions. Openly reporting sustainability data forces companies to reflect on their strengths, weaknesses, and areas for improvement. It acts as a feedback loop, providing valuable insights that can drive positive change within the organization.

![]()

Key Elements of Transparent Sustainability Reporting

A. Data Accuracy and Reliability

- The foundation of transparent reporting is accurate and reliable data. Companies must use credible data sources and robust data collection methods to ensure the integrity of their reports. Independent verification and assurance, conducted by third-party experts, can further enhance the credibility of sustainability data.

B. Clarity and Accessibility

- Sustainability reports should be clear, concise, and accessible to a wide audience. Avoid jargon and technical terms that may confuse readers. Use visuals, such as charts and graphs, to present data in an engaging and easy-to-understand manner. Online platforms and interactive tools can further enhance accessibility.

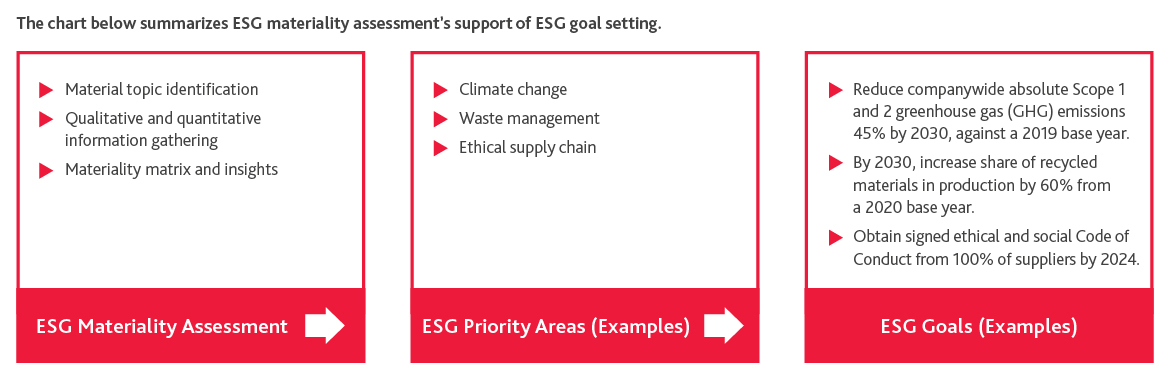

C. Materiality and Relevance

- Materiality is the concept of focusing on issues that are most significant to stakeholders and the company's business. Transparent reporting prioritizes material issues, ensuring that the information disclosed is relevant and meaningful. Companies must engage with their stakeholders to identify and prioritize material topics.

D. Consistency and Comparability

- Using standardized reporting frameworks, such as the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB) promotes consistency and comparability. These frameworks provide guidelines for reporting on a wide range of sustainability topics, ensuring that data is presented in a standardized format. Consistency enables stakeholders to compare performance across different companies and track progress over time.

E. Stakeholder Engagement

- Transparent reporting is a two-way street. Companies must actively seek stakeholder feedback and incorporate it into their reporting processes. Open dialogue and communication are essential for building trust and ensuring that reports meet the needs of all stakeholders.

To enhance transparency in sustainability reporting,

companies should establish clear goals aligned with global standards such as

the Global Reporting Initiative (GRI) Standards.

- Importance

of Clear Goals and Targets:

- Transparent

sustainability reporting involves not just disclosing past performance,

but also outlining future ambitions. This means setting clear,

measurable, and time-bound goals and targets.

- Goals

and targets demonstrate a company's commitment to continuous improvement

and provide a framework for tracking progress.

- They

should be aligned with relevant sustainability frameworks and standards

(e.g., SDGs, science-based targets).

- Characteristics

of Effective Goals and Targets:

- Measurable:

Goals should be quantifiable, allowing for objective assessment of

progress.

- Achievable:

While ambitious, goals should be realistic and attainable.

- Relevant:

Goals should align with the company's material sustainability issues and

stakeholder expectations.

- Time-bound:

Goals should have specific deadlines, creating a sense of urgency and

accountability.

- Transparently

Communicated: Goals and targets, along with the methodologies used to

set them, should be clearly communicated to stakeholders.

EcoTech Solutions' Sustainability Goals and Targets

Context: EcoTech Solutions recognizes its environmental footprint, particularly in energy consumption and e-waste generation. They're committed to improving their sustainability performance and demonstrating transparency.

Goal 1: Reduce Greenhouse Gas Emissions

- Characteristic:

Measurable, Achievable, Relevant, Time-bound, Transparently Communicated

- Target:

Reduce Scope 1 and 2 greenhouse gas emissions by 40% by 2030, compared to

a 2022 baseline.

- Metrics:

Metric tons of CO2e (carbon dioxide equivalent).

- Methodology:

Utilizing the GHG Protocol standards for calculation.

- Transparency:

Progress will be reported annually in the company's sustainability report,

with detailed methodology and data sources.

- Achievable:

EcoTech Solutions will achieve this by transitioning to 100% renewable

energy for their facilities, improving energy efficiency in production,

and reducing transportation emissions.

- Relevant:

This goal aligns with global climate action targets and is a material

issue for the electronics industry.

- Transparent reporting includes regular updates on progress towards goals and targets, including explanations for any deviations.

- Companies should disclose the metrics used to track progress and the assumptions made.

- This allows stakeholders to assess the company's performance and hold it accountable.

Challenges and Solutions to Achieving Transparency

Despite the benefits of transparent reporting, organizations

often face challenges such as complexities in data collection, the risk of

greenwashing (exaggerating or misrepresenting ESG achievements), and

stakeholder skepticism.

A. Challenges

- Data collection and measurement difficulties: Gathering accurate and reliable data can be challenging, especially for complex sustainability issues. For example, a global supply chain company struggles to accurately measure the carbon footprint of its hundreds of suppliers across various countries with differing data collection standards. Or a mining company has difficulty measuring the amount of water used by small, local contractors.

- Lack of standardized reporting frameworks: While frameworks exist, they are not universally adopted, leading to inconsistencies in reporting practices. For example, a small-to-medium enterprise (SME) wants to report its sustainability performance but is overwhelmed by the multitude of frameworks (GRI, SASB, TCFD, etc.) and struggles to choose the most appropriate one. Or, different industries use different metrics to measure the same thing, making cross industry comparison very difficult.

- The complexity of sustainability issues: Sustainability issues are often interconnected and multifaceted, making it difficult to isolate and measure specific impacts. For example: A food company trying to report on its "social impact" has to navigate issues like fair labor practices, community development, and food security, all of which are interconnected and difficult to quantify. Or a chemical company must report on its chemical spills, air emissions, and water contamination, all of which have very different measurement standards.

- The temptation of greenwashing: The pressure to present a positive image can lead to misleading or inaccurate reporting. For example, a clothing brand claims its products are "eco-friendly" based on a small percentage of recycled materials, while ignoring the environmental impact of its overall production process. Or an energy company advertises its small scale solar projects, while heavily investing in fossil fuel extraction.

- The cost of reporting: Implementing robust sustainability reporting systems can be expensive. For example, a small manufacturing company lacks the resources to hire sustainability experts or invest in sophisticated data management systems.

B. Solution

- Investing in robust data management systems: Companies should invest in technology and processes that enable them to collect, analyze, and manage sustainability data effectively.

- Adopting recognized reporting frameworks (GRI, SASB, TCFD): Using established frameworks provides guidance and ensures consistency in reporting practices.

- Seeking independent verification and assurance: Third-party verification enhances the credibility of sustainability reports.

- Prioritizing materiality and relevance: Focusing on material issues ensures that reports are meaningful and relevant to stakeholders.

- Implementing strong governance oversight: Strong governance structures and internal controls can help prevent greenwashing and ensure accurate reporting.

- Embracing digital tools to improve reporting: Digital platforms and tools can streamline data collection, analysis, and reporting.

Case Study Examples

Several companies have set exemplary standards in

transparent sustainability reporting. For instance, Unilever's Sustainable

Living Plan and Microsoft's carbon negative commitment showcase how transparent

reporting can drive positive change while enhancing corporate reputation.

Case Patagonia: Radical Transparency in Supply Chain

- Focus:

Supply chain transparency, environmental impact.

- Action:

Patagonia has made significant efforts to map and disclose its complex

supply chain, revealing both positive and negative impacts. They openly

share information about their factories, materials sourcing, and

environmental footprint, even when it reveals challenges.

- Outcome:

This radical transparency has built strong trust with customers and

stakeholders. While they have faced criticism, their openness has enhanced

their credibility and fostered a culture of continuous improvement.

- Transparency

Element: Data accuracy, clarity, and stakeholder engagement.

Case Unilever: Sustainable Living Plan and Reporting

- Focus:

Comprehensive sustainability goals and reporting.

- Action: Unilever's Sustainable Living Plan set ambitious targets for environmental and social impact. They have consistently reported on their progress, including both successes and setbacks.

- Outcome:

While they faced scrutiny for certain targets, their commitment to

transparent reporting has positioned them as a leader in sustainability.

The company has used the reporting process to drive internal improvements.

- Transparency

Element: Goal and target setting, clarity, and consistency.

Volkswagen "Dieselgate" Scandal: Lack of Transparency

- Focus:

Failure of transparency, negative consequences.

- Action:

Volkswagen intentionally misled regulators and consumers about the

emissions of their diesel vehicles.

- Outcome:

The scandal resulted in significant financial penalties, reputational

damage, and loss of trust. This case highlights the severe consequences of

a lack of transparency.

- Transparency

Element: The absence of all the elements of transparency

These examples illustrate the diverse ways companies approach transparency and the potential consequences of their actions. They emphasize that transparency is not just a reporting exercise but a fundamental aspect of responsible corporate behavior.

The Future of Transparent Sustainability Reporting

The landscape of sustainability reporting is rapidly

evolving. The demand for transparency is growing, driven by increasing investor

and consumer awareness. Technology, such as blockchain and AI, is playing a

growing role in enhancing transparency by providing real-time data and ensuring

data integrity.

Technological advancements like blockchain and data visualization tools offer new avenues for improving the transparency of sustainability reporting. These innovations can enhance data integrity and accessibility, empowering stakeholders to engage more meaningfully with ESG information.

Integrated reporting, which links financial and sustainability performance, is also gaining traction. Furthermore, there is a growing trend towards mandatory sustainability reporting, as governments and regulators seek to standardize reporting practices and hold companies accountable.

Conclusion (Call to Action)

Transparency is not just a buzzword; it's the cornerstone of

credible and effective corporate sustainability reporting. By providing clear,

honest, and accessible information, companies can build trust with

stakeholders, drive accountability, and promote continuous improvement. We

encourage all companies to prioritize transparency in their reporting

practices. Review your current sustainability reporting procedures. Seek

independent verification of your data. Engage actively with your stakeholders.

Learn about GRI and SASB standards, and implement them. By working together, we

can create a future where transparency is the norm, and sustainability is truly

embedded in corporate culture.

Comments

Post a Comment