Navigating ISSB S1 & S2: A Practical Guide for SMEs

Sustainability reporting is no longer just for large corporations. Small and medium-sized enterprises (SMEs) play a critical role in the global economy and supply chains, making their participation essential. The International Sustainability Standards Board (ISSB) has released two key standards: S1 (General Requirements) and S2 (Climate-related Disclosures). This guide is designed to help SMEs understand and practically implement these standards without being overwhelmed.

Overview of ISSB Standards

What is the ISSB? The ISSB develops a comprehensive global

baseline for sustainability disclosures, aiming for consistency and

comparability across industries and borders. Their goal is to ensure that

companies provide sustainability-related information that is relevant for

investment decision-making.

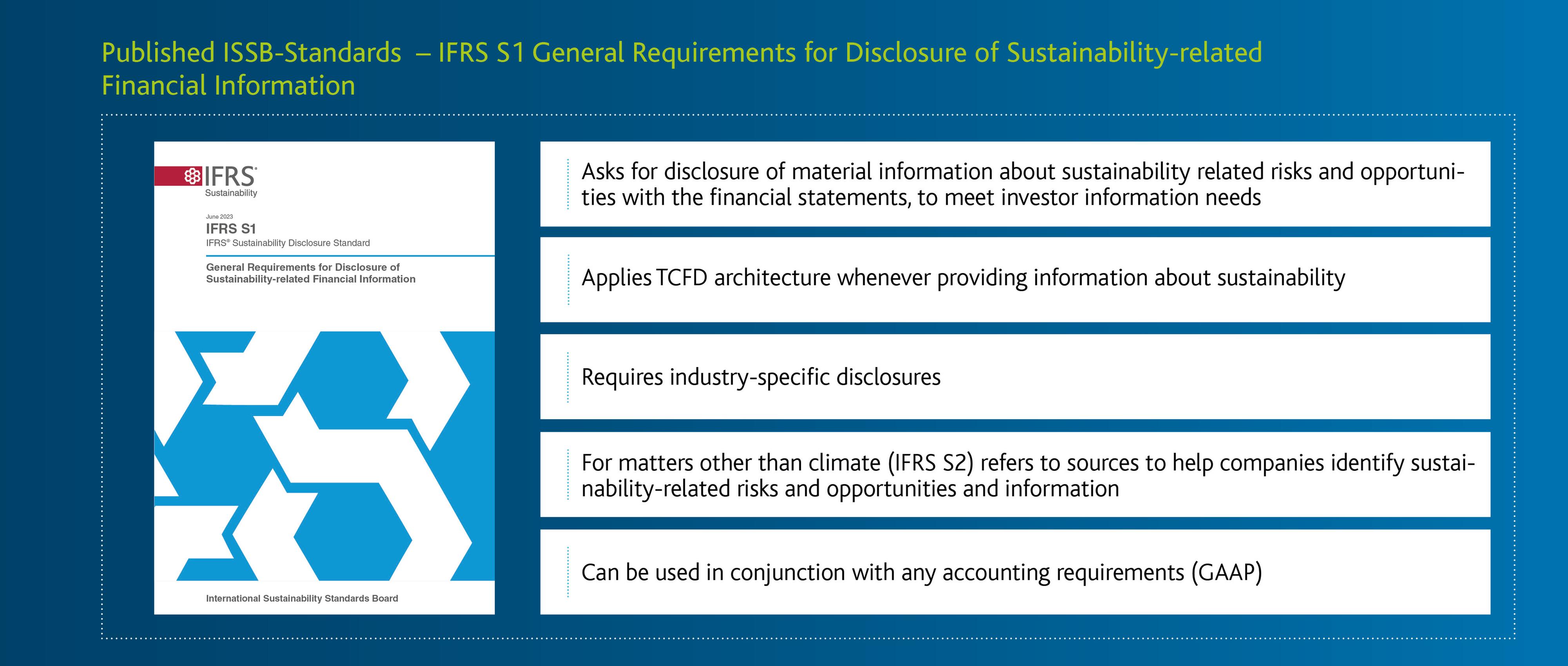

S1: General Requirements for Disclosure of

Sustainability-related Financial Information

- S1

sets out overall requirements for an entity to disclose information about

its sustainability-related risks and opportunities that could reasonably

be expected to affect the entity's cash flows, access to finance, or cost

of capital.

- Disclosures

should cover how these risks and opportunities are governed, managed, and

integrated into overall business strategy.

- The

aim is to ensure that users of financial reports have a full, integrated

view of significant sustainability factors affecting the business.

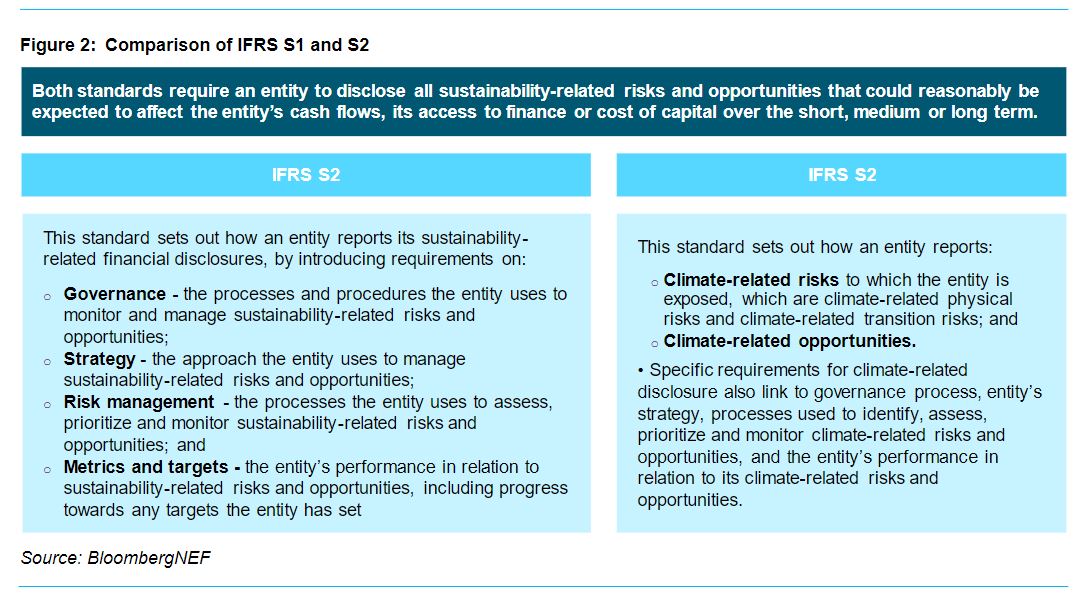

- S2

specifically addresses climate-related risks and opportunities.

- It

is heavily based on the TCFD (Task Force on Climate-related Financial

Disclosures) framework.

- Requires

disclosure under four pillars: Governance, Strategy, Risk Management, and

Metrics & Targets.

- Organizations

must disclose their greenhouse gas emissions, transition plans,

climate-related scenario analyses, and the resilience of their strategies

under different climate scenarios.

- Consistency:

Reports should be comparable over time and between organizations.

- Comparability:

Enables stakeholders to compare sustainability data between similar

organizations.

- Reliability:

Information should be verifiable and based on sound data and governance.

- Materiality:

Focus on information that significantly influences decisions made by users

of general-purpose financial reporting.

- Connectivity of Information: Sustainability disclosures

should be linked clearly with the entity's general financial reporting.

These principles ensure that sustainability reporting is not just an

additional document but integrated into the overall understanding of a

company's financial health and future prospects.

Key Challenges for SMEs

Small and medium-sized enterprises (SMEs) often face unique barriers when

trying to adopt sustainability reporting standards like ISSB S1 and S2. Key

challenges include:

- Limited Resources (Time, Budget,

Expertise)

Most SMEs operate with lean teams and tight budgets, making it difficult to dedicate staff or hire external consultants for sustainability reporting. Sustainability responsibilities are often added on top of existing roles rather than assigned to specialized personnel. - Data Availability and Quality

SMEs may not have robust systems in place to collect, track, and validate environmental, social, or governance data. Critical data such as greenhouse gas emissions, energy consumption, or climate-related risks might not be consistently monitored or may be spread across different departments without integration. - Technical Complexity of Standards

The ISSB Standards, although meant to be accessible, still use technical language and concepts (like scenario analysis or transition risks) that can be overwhelming for SMEs unfamiliar with sustainability frameworks. - Materiality Assessment

Difficulties

Determining what is “material” for reporting purposes can be challenging without formal processes or external guidance. SMEs may lack experience in engaging stakeholders systematically to validate material topics. - Balancing Short-term and

Long-term Priorities

SMEs often prioritize immediate operational survival and financial performance over longer-term sustainability strategy, especially during periods of economic uncertainty. - Fear of Public Disclosure

Some SMEs worry that revealing environmental or climate weaknesses might harm their reputation, deter investors, or create legal risks, even if early-stage reporting is encouraged and transparency is viewed positively in the long run.

Practical Tips for Overcoming Challenges

- Start Small: Focus initially on one or two

material topics rather than trying to report comprehensively from the

outset.

- Use Existing Data: Leverage operational data you

already collect (e.g., electricity bills, fuel usage) to begin tracking

sustainability metrics.

- Simplify Language: Avoid overcomplicating your

report; use clear and direct language.

- Seek External Support: Tap into free online tools,

industry associations, or government initiatives offering SME

sustainability resources.

- Engage Stakeholders Early: Even simple surveys or informal

discussions with customers, suppliers, or employees can provide valuable

insights.

- Prioritize Transparency Over

Perfection: Stakeholders appreciate honest disclosure, even if some areas are

still under development.

Implementation Roadmap for SMEs

Step 1: Understand the Basics

Before starting, SMEs need a firm grasp of what S1 and S2 require. Focus

on the four main pillars:

- Governance: Disclose who is responsible for

managing sustainability risks and opportunities. This could include board

oversight, management responsibilities, and reporting lines. Example: A small food company, GreenBite

Foods, assigned its CFO to oversee sustainability governance,

reporting quarterly to the board about climate-related risks and

initiatives.

- Strategy: Explain how sustainability

risks and opportunities affect business strategy and financial planning.

Describe any changes in business models or adaptations to climate-related

risks. Example: EcoLogix

Builders, an SME in construction, incorporated climate adaptation

(like flood-resilient designs) into its new product offerings to address

risks from increased severe weather events.

- Risk Management: Share how sustainability and

climate risks are identified, assessed, and managed. Integrate these risks

into the enterprise risk management system. Example: SolarEdge Tech, a

renewable energy SME, conducted a simple risk mapping exercise to assess

how supply chain disruptions from extreme weather could affect its solar

panel installations.

- Metrics and Targets: Report quantitative and

qualitative metrics that track sustainability risks and opportunities. Set

and disclose targets where possible (e.g., carbon reduction goals). Bloom Packaging, an SME

manufacturer, started tracking electricity use monthly and set a goal to

reduce energy consumption by 10% within two years.

Sample Reporting Template

|

Pillar |

What to Disclose |

Example Prompts for SMEs |

Example from SMEs |

|

Governance |

Who oversees sustainability? How often do they review it? |

- Who is responsible? |

CFO reports quarterly to the Board on sustainability matters. |

|

Strategy |

How sustainability risks and opportunities affect the business |

- Has climate change affected your business plan? |

Building flood-resilient houses to address extreme weather impacts. |

|

Risk Management |

How risks are identified, assessed, and managed |

- How do you assess risks like climate change? |

Conducted a risk workshop with department heads to map climate risks. |

|

Metrics and Targets |

What you measure and what goals you set |

- What data do you track (e.g., energy use)? |

Set a target to reduce electricity consumption by 10% over two years. |

Step 2: Set Internal Foundations

To build a strong starting point for sustainability reporting, SMEs need

to set internal foundations by establishing responsibility, identifying what

matters most (materiality), and preparing a basic reporting process.

- Assign Responsibility

Even if you don't have a dedicated sustainability officer, assign a specific person or small team to oversee sustainability reporting. This individual should coordinate data collection, stakeholder engagement, and communication with leadership. - Conduct a Materiality Assessment

A materiality assessment helps you figure out which sustainability topics are most important to your business and stakeholders.

How SMEs can do it simply:

- List potential sustainability

topics (e.g., carbon emissions, waste management, supply chain ethics).

- Identify key stakeholders (e.g.,

customers, employees, suppliers) and ask them — even informally — which

issues they care about most.

- Prioritize topics based on two

factors:

- How much they affect your

business success (financial impact, operational risk)

- How much they matter to your

stakeholders

- Plot these topics on a simple materiality

matrix (high/low importance to business vs. stakeholders).

- Select the top few topics for

your first report.

Example:

A small logistics company found that "fuel efficiency" and

"driver safety" were the top material issues after surveying

employees and reviewing customer feedback.

- Create a Basic Reporting

Framework

Define a simple process for reporting:

- When: Set a reporting timeline

(e.g., annually).

- What: Agree on the scope of

disclosures (e.g., energy use, climate risk strategy).

- How: Assign internal checkpoints

(e.g., mid-year progress reviews) and decide on external publishing

formats (e.g., a section in the annual report, a standalone

sustainability report).

Setting a strong internal foundation ensures that sustainability reporting is

organized, focused on the right topics, and manageable even with limited

resources.

Step 3: Climate Risk and Opportunity Identification (S2)

Imagine this: You're running a thriving local bakery, renowned for your

delicious sourdough. Suddenly, a severe heatwave scorches your wheat supplier's

fields, causing a shortage. Flour prices skyrocket, threatening your profit

margins. This is a climate risk—a direct impact of climate change

on your business. This isn't just a hypothetical scenario; climate change is

already impacting businesses of all sizes.

The ISSB's S2 standard asks businesses to identify these risks and opportunities. It's not about doom and gloom; it's about smart business planning.

- Identify Physical Risks: Assess how climate change (e.g., floods, heatwaves) could directly impact operations, supply chains, and infrastructure. Start by considering the location of your business, your suppliers, and your customers. Are they vulnerable to specific climate hazards? What are the potential impacts on your operations and finances. For example, a bakery might experience supply chain disruptions if its wheat supplier is affected by drought, or a construction company might face delays if its projects are impacted by extreme rainfall.

- Identify Transition Risks: Evaluate how policy shifts, technology changes, and evolving customer preferences related to a low-carbon economy might affect the business. Consider your industry and your competitors. Are they making changes to address climate change? How are your customers responding to these changes? What are the potential implications for your business? For example, a car repair chain might need to adapt to servicing electric vehicles. Evolving customer preferences, such as a growing demand for sustainable products, can create new market opportunities or make existing products less appealing. For example, a clothing retailer might need to offer more eco-friendly clothing options to attract environmentally conscious customers.

- Spot Opportunities: Recognize new business models,

products, and services that arise from the move towards a sustainable

economy (e.g., energy efficiency products). What are the unique challenges

and opportunities in your industry? How can you adapt your business model

to capitalize on the transition to a sustainable economy? For example, a

plumbing company could offer water-saving solutions, a construction

company could specialize in energy-efficient buildings, or a software

company could develop tools for carbon accounting.

Step 4: Collect and Organize Data

Collecting sustainability data might seem daunting, but it doesn't have to be. Start small, focus on what's readily available, and build from there.- Start with Easy Wins: Track available data like electricity usage, business travel emissions, or resource consumption. These "easy wins" provide a quick way to demonstrate progress and build momentum.

- Electricity Usage: This is usually readily available from your utility bills. Track your monthly or annual electricity consumption. This data forms the basis for calculating your Scope 1 emissions (direct emissions from your operations).

- Business Travel Emissions: If your employees travel for work, track the distance and mode of transportation (flights, cars, trains). Use online carbon calculators to estimate the emissions associated with these trips. This contributes to Scope 1 emissions.

- Resource Consumption: This could include water usage (from utility bills), paper consumption (track office supplies), or waste generation (weigh or estimate waste produced). This data is vital for assessing your environmental impact and identifying areas for improvement.

- Supplier Data: Start by collecting data from your key suppliers. Ask them about their sustainability practices and whether they can provide information about their carbon footprint or other relevant metrics.

- Use Templates and Tools: Implement simple spreadsheets or software tools to organize and store sustainability-related data.

- Spreadsheets: A spreadsheet program (like Google Sheets or Microsoft Excel) is a great starting point. Create simple templates to track your data consistently over time. You can use formulas to calculate totals, averages, and other relevant metrics.

- Free Sustainability Software: Explore free or low-cost sustainability software solutions designed for SMEs. These tools often provide templates, calculations, and reporting features to streamline the data collection and analysis process. Many offer free versions suitable for small businesses.

- Dedicated Sustainability Platforms: As your business grows and your data collection becomes more complex, consider using a dedicated sustainability platform. These platforms offer more advanced features, such as data integration, reporting, and benchmarking. However, these are usually paid services.

- Standardize Data Collection: Develop templates that allow data to be consistently gathered across departments and over time.

- Templates: Create clear and concise templates for each data point you're tracking. Ensure that everyone in your organization understands how to use the templates and what information needs to be collected. This consistency is crucial for accurate reporting.

- Data Definitions: Clearly define what each data point represents. For example, specify the units of measurement (kilowatt-hours for electricity, liters for water, kilograms for waste). This eliminates ambiguity and ensures accurate data entry.

- Data Entry Procedures: Establish clear procedures for data entry and storage. This might involve designating a specific person or department responsible for collecting and entering the data. Regular data checks and validation help to maintain data accuracy.

- Regular Data Reviews: Schedule regular reviews of your collected data to ensure its accuracy and completeness. Identify and correct any errors or inconsistencies. This ongoing review is essential for maintaining data quality.

Step 5: Draft the First Report

Creating your first sustainability report can feel overwhelming, but by breaking it down into manageable steps and focusing on clarity, you can create a compelling narrative that showcases your commitment to sustainability.

- Structure Around the Four Pillars: Organize the report according to Governance, Strategy, Risk Management, and Metrics & Targets.

o Governance: This section describes your organization's structure, leadership commitment to sustainability, and the processes in place to oversee sustainability initiatives. Include information about your board's oversight of sustainability, the roles and responsibilities of key personnel, and your commitment to ethical business practices.

o Strategy: Outline your overall sustainability strategy, including your goals, objectives, and key priorities. Explain how sustainability is integrated into your business strategy and operations. This section should demonstrate your long-term vision and commitment to sustainability.

o Risk Management: Describe your approach to identifying, assessing, and managing sustainability-related risks and opportunities. This should include your process for identifying material topics, assessing their potential impacts, and developing mitigation strategies. For SMEs, focus on the most relevant risks, such as supply chain disruptions or changes in customer preferences.

o Metrics & Targets: Present key performance indicators (KPIs) and targets related to your sustainability performance. Focus on metrics that are relevant to your business and that you can easily track. For example, you might track your energy consumption, waste generation, or greenhouse gas emissions. Include your targets for reducing your environmental impact and improving your social and governance performance.

- Be Transparent and Honest: Clearly state what is being reported, what is in progress, and where there are gaps. Acknowledge any limitations in your data. Explain the methods you used to collect and analyze your data, and highlight any uncertainties or assumptions. Transparency about data gaps demonstrates integrity.

- Keep It Simple: Avoid jargon and focus on making the report understandable to a broad audience. Use clear and concise language, avoiding technical terms or acronyms that might not be understood by everyone. Use charts, graphs, and other visual aids to present your data in an engaging and accessible way. Use storytelling to bring your sustainability journey to life. Share examples of how you've implemented sustainability initiatives and the positive impacts they've had.

- Use a Checklist: Review the final draft against a simple checklist to ensure that all necessary S1 and S2 requirements have been addressed.

- S1 Checklist: Ensure that you've adequately addressed the general requirements for disclosure, including materiality, double materiality, and the connection between sustainability and financial performance.

- S2 Checklist: Ensure that you've addressed climate-related risks and opportunities, including physical and transition risks. Include relevant metrics and targets.

- Overall Checklist: Review the entire report to ensure that it's clear, concise, accurate, and consistent with your organization's sustainability strategy.

By following these steps, SMEs can create a compelling sustainability

report that showcases their commitment to sustainability, builds trust with

stakeholders, and meets the core requirements of ISSB S1 and S2. Remember, your

first report is a starting point. Continuous improvement and refinement are key

to building a strong sustainability reporting practice.

Step 6: Your Toolkit: Practical Tools and Templates

This section provides practical tools and templates to help you navigate

the process of identifying material topics, assessing climate risks, tracking

emissions, and ensuring your report meets the necessary requirements. Remember,

these are starting points; adapt them to your specific needs.

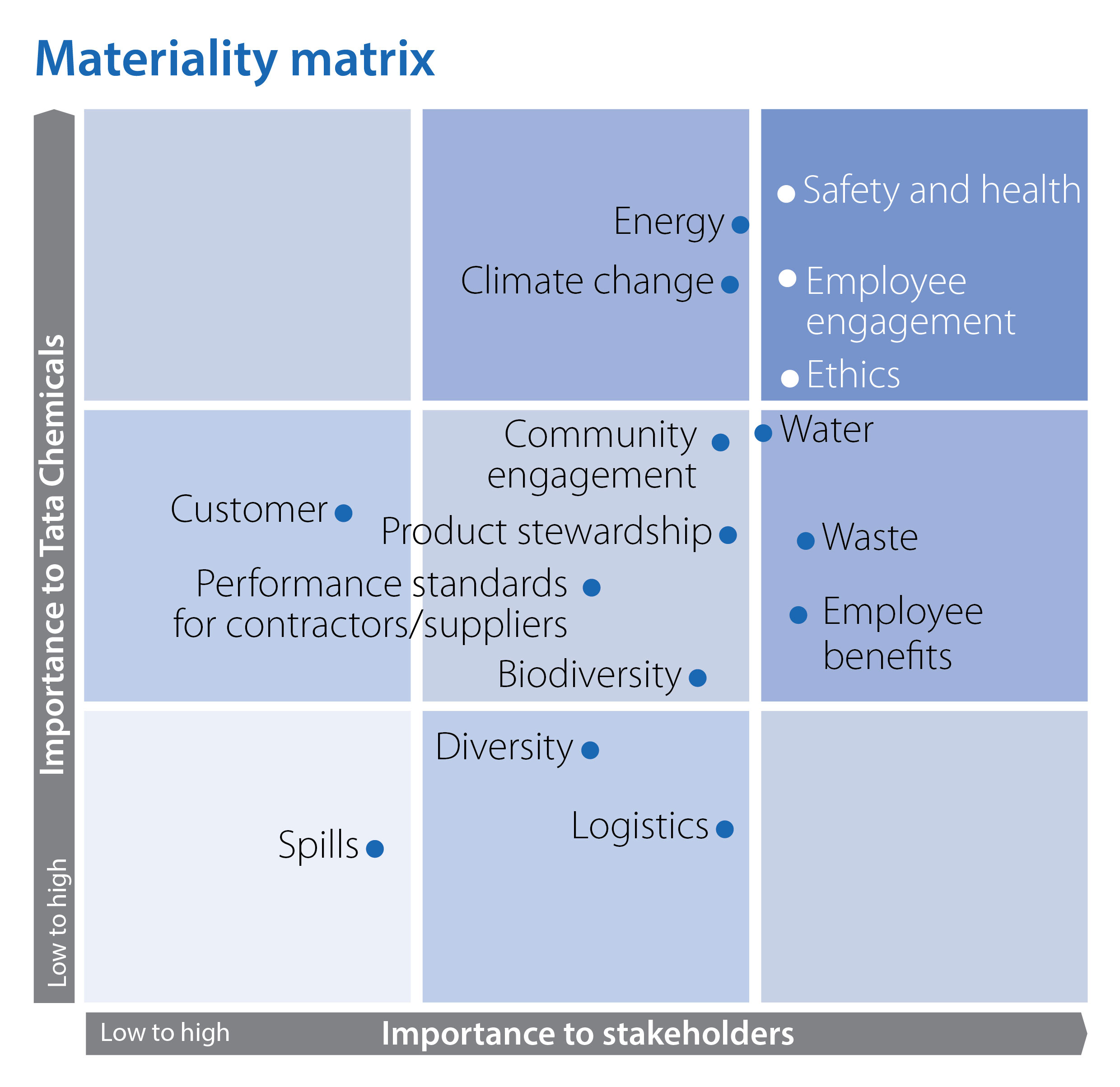

A. Materiality Matrix: Prioritizing What Matters Most

A materiality matrix helps you prioritize the economic, environmental,

and social issues most significant to your business and stakeholders. A simple

matrix can be created using a spreadsheet:

- List potential topics: Brainstorm potential

sustainability topics relevant to your business (e.g., energy use, waste

generation, employee satisfaction, supply chain impacts).

- Identify stakeholders: List your key stakeholders

(e.g., investors, customers, employees, community).

- Rate significance: For each topic, rate its

significance to your business and to each stakeholder group on a scale

(e.g., 1-5, low to high).

- Plot on matrix: Plot each topic on a matrix

with "Significance to Business" on one axis and

"Significance to Stakeholders" on the other.

- Prioritize: Topics in the high-significance quadrants are your material topics. Focus your reporting efforts on these.

B. Climate Risk Register: Mapping Your Climate Vulnerabilities

A climate risk register helps you systematically identify, assess, and

manage climate-related risks. Use a spreadsheet to create a register with

columns for:

- Risk Description: A clear description of each

climate-related risk (e.g., increased energy costs, supply chain

disruptions due to extreme weather).

- Likelihood: The probability of the risk

occurring (e.g., low, medium, high).

- Impact: The potential consequences

of the risk (e.g., financial losses, reputational damage).

- Vulnerability: Your business's

vulnerability to the risk.

- Mitigation Strategies: Actions you can take to

reduce the likelihood or impact of the risk.

- Responsibility: Who is responsible for

managing each risk?

- Timeline: When will the mitigation

strategies be implemented?

C. Emissions Calculator: A Simple Spreadsheet for Tracking Scope 1 and 2 Emissions

A simple spreadsheet can help you track your Scope 1 (direct emissions

from your operations) and Scope 2 (indirect emissions from purchased energy)

emissions. Include columns for:

- Emission Source: (e.g., electricity

consumption, business travel, purchased fuels).

- Quantity: (e.g., kilowatt-hours,

miles driven, liters of fuel).

- Emission Factor: (Obtain emission factors

from relevant sources; many online calculators provide these).

- Total Emissions: (Quantity x Emission

Factor).

Sample worksheet of Emission Calculations

A checklist helps ensure your report covers all necessary aspects of ISSB

S1 and S2. Create a checklist based on the specific requirements of the

standards, including sections such as:

- Governance: Board oversight, roles and

responsibilities, ethical business practices.

- Strategy: Sustainability goals,

objectives, and key priorities.

- Risk Management: Climate-related risks and

opportunities, mitigation strategies.

- Metrics and Targets: Key performance indicators

(KPIs), emissions data, targets for reduction.

- Stakeholder Engagement: How you engaged with

stakeholders in the reporting process.

Implementing ISSB S1 and S2 standards may seem daunting at first, but SMEs should focus on progress over perfection. Transparency, even if limited in scope initially, positions SMEs as responsible and forward-looking organizations, capable of thriving in a sustainability-driven economy.

Comments

Post a Comment